Land transport consumes around 50% of global oil, and increasing car ownership suggests demand for oil will continue to grow. Photo by Davide Gabino/Flickr

Global carbon dioxide emissions from fossil fuels are on track to again climb to a record high in 2019, according to a new report from the Global Carbon Project, putting the world at risk of catastrophic climate change due to these heat-trapping gases. This is further evidence that the plateau in emissions growth between 2014 and 2016 was short-lived: emissions from fossil fuels grew 1.5% in 2017, 2.1% in 2018 and are projected to grow another 0.6% in 2019. This growth is at odds with the deep cuts urgently needed to respond to the climate emergency.

The alarming news was released as almost 200 nations gathered in Madrid, Spain, to finalize rules of the Paris Agreement on climate change and prepare to enhance their national climate commitments in 2020.

Here are six takeaways from the report and accompanying analyses, which offer more detailed insights into the data. The data can also be explored in depth on WRI’s Climate Watch data platform.

1. Another Year of Growing Emissions

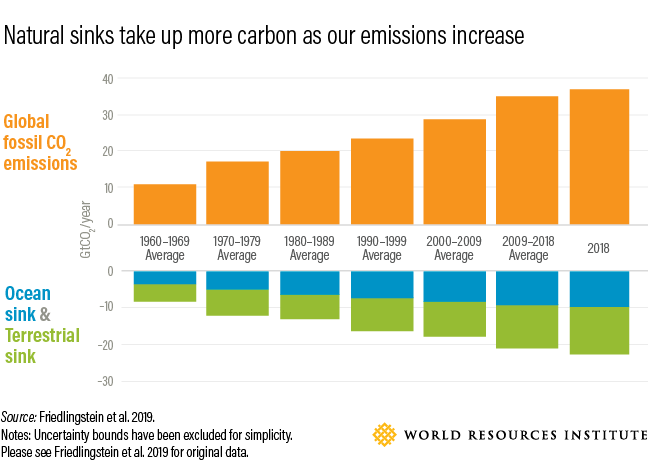

For the first time, fossil fuel carbon emissions hit 10 gigatons per year in 2018 (or, just under 37 gigatons carbon dioxide), more than double the level in the 1970s.

In developed countries where emissions have already peaked, carbon dioxide emissions aren’t dropping quickly enough to offset emissions growth elsewhere. Emissions in 2019 are expected to decline in both the European Union and United States by 1.7%, as India’s emissions are expected to rise 1.8% (notably lower than the past five-year growth rate of 5.1%), China’s are expected to rise 2.6% and emissions in the rest of the world are expected to rise 0.5%.

Average per capita emissions were 4.8 tonnes of fossil fuel carbon dioxide per person last year. This number was considerably higher in Australia (16.9 tonnes per person), China (7.0 tonnes per person), the EU (6.7) and the United States (16.6). Notably, China’s per capita carbon dioxide emissions are now higher than those of the EU (although historically they were not), while India’s per capita emissions (2.0 tonnes per person) are about one eighth of those of the U.S.

2. Oceans and Land are Soaking Up More Carbon Dioxide

Land and oceans – our carbon sinks – are continuing to soak up carbon dioxide at a rate that tracks the rise of carbon dioxide concentration in the atmosphere, partly compensating for the growth in emissions. The global ocean has taken in 2.5 gigatons per year in the last decade, more than double what it did in the 1960s. Lands took in 3.2 gigatons per year in the last decade, more than 1.5 times the rate in the 1970s.

But our ocean and land sinks could be compromised by future warming, which could limit the amount of carbon dioxide they absorb, making global temperatures rise even faster than they are now.

3. Coal Is on a Clear Decline, but Still Dominates Emissions

Coal is the largest contributor of fossil fuel carbon dioxide emissions, making up 42% of the global total. However, as renewable or lower-emissions power sources become more economically competitive and more countries turn away from coal due to its impact on climate and health, there are signs that coal is clearly in decline. U.S. generation from coal is projected to decline 11% from 2018 to 2019 to a level that has not been witnessed for more than 50 years, about half of what its peak was in 2005. In Europe, coal-based emissions declined 10% in 2019. And in the UK, coal has dropped from 42% in 2012 to only 5% of electricity generation in 2018.

At the same time, coal use is increasing elsewhere to meet energy demand, although more slowly than in the past. In China, coal use is expected to increase by 0.8% this year, with a decline of coal use in the power sector and lower growth in industrial production. In India, carbon dioxide emissions from coal are anticipated to grow by 1.8% this year, less than half the average growth rate of the last five years.

4. Natural Gas, the Fastest-growing Fossil Fuel, Doesn’t Always Replace Coal

Globally, the use of natural gas rose an average of 2.6% per year over the past five years and its emissions are expected to increase 2.5% in 2019. Even with this rapid growth, it contributes around half the emissions of coal.

Previously dependent on pipelines for transport, natural gas markets are becoming more global as liquified natural gas (LNG) markets grow – LNG trade is up 10% in 2018 alone. This is reducing regional price differences and driving demand where prices are dropping, mainly in Asia.

While natural gas is sometimes considered a bridge fuel between coal and renewables because it emits about half the carbon dioxide of coal, the investments being made now in natural gas infrastructure will lock in its use and its emissions for decades to come, potentially delaying the shift to lower carbon sources. For example, in 2019, the U.S. Federal Energy Regulatory Commission has approved 11 LNG export projects.

Most critical to watch is whether natural gas is replacing or adding to coal use. So far, replacement appears to be happening in some major markets, like the United States, but not in others, like Japan, where it is substituting for lost nuclear power

5. Oil Is on the Rise, Driven by Increasing Demand for Transport

As with natural gas, oil use also continues to increase globally, up an average of 1.9% per year over the last decade and making up just over a third of global fossil fuel emissions. Around half of oil is used in land transport, with demand rising in developing and many developed countries. In the United States there is already nearly one vehicle per person, while in many developing markets this ratio is far lower, with one vehicle for every six people in China and one for every 40 people in India. Projections for increasing private vehicle ownership in China, India and other developing markets suggest demand for oil will continue to grow for years to come.

Airline travel, while representing only 8% of emissions from global oil use, is also growing. The number of passenger trips is up 7% per year on average from 2013 through 2018 and shows potential to continue, especially in developing countries where per capita use of airline travel remains comparatively low.

6. Solutions Exist

A number of approaches can be used to decarbonize economies, including replacing fossil fuels with renewables and setting fuel efficiency standards. As at least 18 countries have shown, national emissions levels can fall as economies grow. What’s needed is the commitment by more countries to do so and transform their economies for rapid decarbonization.

The COP25 Opportunity

This month’s international climate conference, COP25, in Madrid, provides a key opportunity for countries to signal that they will increase the ambition of their national climate commitments, known as nationally determined contributions or NDCs. Sixty-eight already have indicated they will enhance their NDCs in 2020, but they represent only 8% of global emissions. Major emitters need to step forward and lead the world.

While this year’s report indicates a lower growth rate than the past few years, even zero growth in emissions is not enough. Furthermore, on top of rising emissions during the past few years, preliminary data estimates for 2020 suggest that emissions will continue to increase next year. We need to actively bend the emissions curve downwards to have any hope of being on track for a world that is well below 2 degrees C (3.6 degrees F) and ideally less than 1.5 degrees C (2.7 degrees F) warmer than before the Industrial Revolution. Only by getting emissions growth below zero can we realistically expect to avoid the most severe impacts of climate change.

Editor’s note: Updated with information from WRI’s Climate Watch data platform.

This blog was originally published on WRI’s Insights.

is a Senior Associate with the Global Climate Program at World Resources Institute.

is a Research Analyst II for the Climate Program at World Resources Institute.